What Is Tax-Ready Bookkeeping? A Guide for Small Businesses

Tax-ready bookkeeping is defined as the practice of maintaining business financial records that are accurate, reconciled, and supported by documentation so they can be used directly for tax preparation without cleanup. For small business owners and freelancers, this means your books reflect real transactions, every account ties out, and every deduction has a receipt behind it. The IRS expects records that clearly show income and expenses and can be accessed at any time. When your bookkeeping meets that standard year-round, tax season becomes a reporting exercise rather than a recovery project.

What is tax-ready bookkeeping, and what practices define it?

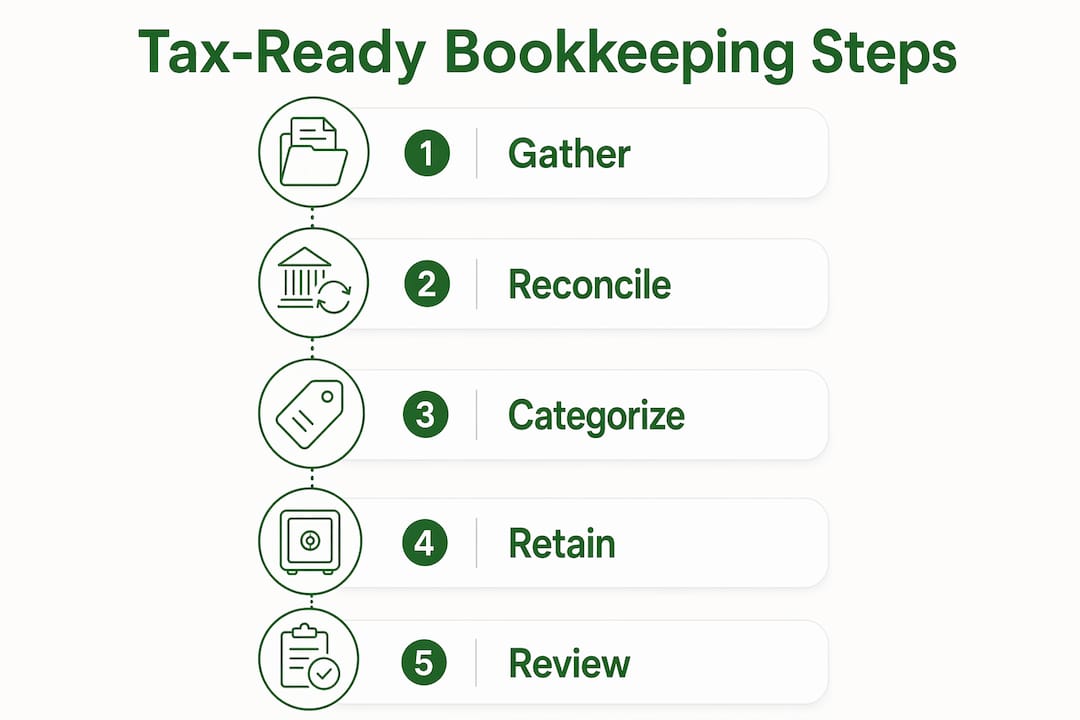

Tax-ready bookkeeping means your books are complete, reconciled, and correctly categorized with no missing or guessed entries. That definition has four working parts, each of which carries real weight during tax preparation.

The first is reconciliation. Every bank account, credit card, and loan account must be reconciled against external statements. Reconciliation confirms that what your books show matches what actually moved through your accounts. Skipping this step is the single most common reason books require cleanup before a CPA can file.

The second is consistent transaction categorization. Each transaction must be assigned to the correct category aligned with tax reporting, such as IRS Schedule C line items for sole proprietors. Miscategorized expenses either inflate deductions you cannot defend or bury deductions you legitimately earned.

The third is supporting documentation. Receipts, invoices, and contracts must exist and connect clearly to the transactions they support. Supporting documents must demonstrate business purpose and enable a third party to understand why a transaction occurred.

The fourth is separation of personal and business finances. Mixing personal purchases into a business account creates a categorization problem that cascades through every report. A dedicated business checking account and credit card eliminates most of this risk before it starts.

- Reconcile every account monthly, not just at year-end

- Assign each transaction a category at the time of entry, not retroactively

- Attach receipts or invoices directly to transactions in your records

- Keep personal and business accounts completely separate

- Never estimate or guess a transaction amount; find the source document

Pro Tip: Complete month-by-month reconciliations before making adjusting entries to prevent double counting and timing errors that compound over the year.

How does tax-ready bookkeeping reduce tax preparation stress and errors?

Clean books eliminate the bottleneck that slows most tax filings. When your accountant receives reconciled records with proper categorization, they can prepare your return without reclassifying transactions or rebuilding transaction histories from scratch. Tax-ready books reduce delays and last-minute issues by removing the cleanup phase entirely.

The practical difference shows up in several ways:

- Fewer questions from your CPA about unexplained transactions

- No missed deductions because expenses were never recorded

- Reduced audit risk because every entry has a supporting document

- Faster turnaround on your return, which matters when you owe or expect a refund

- Lower accounting fees because preparers bill by time, and clean books take less of it

The audit risk point deserves emphasis. The IRS does not audit randomly. Patterns that trigger scrutiny include large deductions without documentation, income that does not match third-party reports, and inconsistent categorization across years. Tax-ready records address all three by creating a consistent, documented financial narrative.

Tax-ready books provide a defensible financial narrative that enables accountants to efficiently finalize tax returns with fewer disruptions. Properly prepared books reflect income and expenses correctly, are reconciled for reliability, and prevent last-minute reconstruction that introduces errors.

Pro Tip: Continuous upkeep throughout the year prevents the year-end scramble. Thirty minutes of bookkeeping per week is far less painful than three days of reconstruction in April.

What IRS recordkeeping requirements align with tax-ready bookkeeping?

The IRS does not prescribe a specific software or format. Any recordkeeping system is acceptable as long as it clearly shows income, expenses, and the supporting documents that substantiate your tax return entries. That flexibility is good news for freelancers and small business owners who use spreadsheets, basic accounting software, or even organized paper files.

What the IRS does require is that records be organized, accessible, and retained for the appropriate period. For most business records, the standard retention period is three years from the filing date, though records related to property or employment taxes carry longer requirements.

Tax-ready bookkeeping satisfies IRS expectations because it is built around the same principles the IRS uses to evaluate returns. Records must be maintained and accessible at all times for potential review, not just assembled at filing time. The table below summarizes the core record categories the IRS expects small businesses to maintain.

| Record Category | Examples of Required Documents |

|---|---|

| Income | Sales receipts, invoices, bank deposit records, 1099 forms |

| Business expenses | Receipts, canceled checks, credit card statements, vendor invoices |

| Assets | Purchase records, depreciation schedules, improvement costs, sale records |

| Payroll | W-2s, payroll registers, tax deposit records, employee timesheets |

| Travel and meals | Receipts with date, amount, business purpose, and attendees noted |

Each category maps directly to a section of your tax return. When your books are organized by these categories throughout the year, pulling the data for filing is a matter of export rather than excavation.

How to build and maintain tax-ready bookkeeping for your business

Building tax-ready books is not a one-time project. It is a set of repeatable habits that keep your records current and reliable. A stable chart of accounts aligned to tax requirements minimizes year-end corrections by ensuring every transaction lands in the right place from the start.

Establish a chart of accounts tied to tax categories. Map your income and expense accounts directly to the tax lines you will report on. For sole proprietors, that means Schedule C categories. For S-corps or partnerships, align to the relevant return. This prevents reclassification at year-end.

Reconcile every account at month-end. Set a fixed date each month, such as the fifth business day after the prior month closes, to reconcile all bank and credit card accounts. Treat it as a non-negotiable deadline, not an optional task.

Attach documentation at the point of entry. When you record a transaction, attach the receipt or invoice immediately. Digital tools that allow photo attachments to individual transactions make this practical even for mobile-first freelancers.

Review categorization before each quarter closes. Spend 20 minutes before the end of March, June, September, and December scanning your transaction list for miscategorized entries. Catching errors quarterly is far easier than untangling a full year in January.

Schedule a mid-year bookkeeping review. A mid-year check with your accountant surfaces issues while there is still time to correct them. Year-end checklists that include reconciled accounts, financial statements, and payroll summaries confirm readiness before the filing deadline arrives.

Keep personal and business finances permanently separate. Open a dedicated business checking account and credit card if you have not already. Every transaction on those accounts is presumptively business-related, which simplifies categorization and documentation.

Pro Tip: Regular communication with your accountant keeps your books aligned with tax prep needs. A 15-minute quarterly call costs far less than a full cleanup engagement in February.

Common misconceptions about tax-ready bookkeeping

Tax-ready bookkeeping does not mean perfect bookkeeping. Tax-ready is focused on clarity and usability, not flawless records. A small business owner who tracks income consistently, categorizes expenses correctly, and keeps receipts has tax-ready books. A freelancer who reconciles monthly but occasionally rounds a small expense to the nearest dollar does not have a compliance problem.

Several myths prevent small business owners from engaging with bookkeeping at all:

- "I need expensive software." The IRS accepts any organized system. A well-maintained spreadsheet with consistent categories and attached receipts meets the standard.

- "My accountant handles all of this." Tax preparers prepare returns. Bookkeepers maintain records. These are different roles. Your accountant cannot file an accurate return from a shoebox of receipts.

- "Tax-ready means audit-proof." No set of records guarantees immunity from audit. Tax-ready records do mean that if an audit occurs, you can respond with documentation rather than reconstruction.

- "I only need records during tax season." The IRS can review returns for up to three years after filing. Records must be accessible year-round, not just in april.

The practical standard is straightforward: every transaction should have a category, a source document, and a clear business purpose. That traceability is what the IRS looks for, and it is what your accountant needs to file accurately.

Key Takeaways

Tax-ready bookkeeping is a year-round practice of reconciling accounts, categorizing transactions correctly, and retaining supporting documents so that tax preparation requires no cleanup and every deduction is defensible.

| Point | Details |

|---|---|

| Definition of tax-ready | Books are complete, reconciled, and categorized with no missing or guessed entries. |

| IRS recordkeeping standard | The IRS requires organized, accessible records by category, not a specific software or format. |

| Year-round discipline | Tax-ready bookkeeping is maintained continuously, not assembled at filing time. |

| Documentation quality | Every transaction needs a receipt or invoice that clearly shows its business purpose. |

| Practical benefit | Clean books reduce accounting fees, audit risk, and missed deductions at tax time. |

Why I think most small businesses approach this backwards

Most small business owners treat bookkeeping as a tax-season obligation. They collect receipts in a folder, hand everything to an accountant in february, and hope for the best. That approach works until it does not, and when it fails, the cost is real: cleanup fees, missed deductions, and the stress of reconstructing a year of transactions under deadline pressure.

What I have observed consistently is that the businesses with the least tax-season stress are not the ones with the most sophisticated software. They are the ones with the simplest, most consistent habits. Monthly reconciliations. Receipts attached at the time of purchase. A chart of accounts that has not changed in three years. That consistency is what makes books tax-ready.

The mindset shift that matters most is treating bookkeeping as a financial management tool rather than a compliance chore. When your records are current and accurate, you can see your actual profit margin in real time, make informed decisions about expenses, and walk into a conversation with your accountant or a lender with confidence. Tax readiness is a byproduct of good financial management, not a separate project.

Start with one habit: reconcile every account on the same date each month. Build from there. Perfection is not the goal. Clarity and consistency are.

— Ian

How Taxbatchpro supports your tax-ready bookkeeping workflow

Maintaining tax-ready financial records requires accurate, structured transaction data. Taxbatchpro converts scanned bank and credit card statement PDFs into structured Excel spreadsheets, with transactions automatically mapped to IRS Schedule C categories. That means less time on manual data entry and more confidence that your records are organized the way your accountant and the IRS expect.

Freelancers and small business owners can process a full year of statements in under 90 seconds. Accountants working with multiple clients use the statement extraction tools to eliminate manual transcription entirely. For a closer look at what the platform offers, the IRS-ready conversion page walks through exactly how the process works. Taxbatchpro also offers a free PDF to Excel converter as an entry point for business owners who want to see the output before committing.

FAQ

What is tax-ready bookkeeping in simple terms?

Tax-ready bookkeeping means your business financial records are reconciled, correctly categorized, and supported by documentation so a tax preparer can file your return without needing to clean up or reconstruct your books first.

Does the IRS require specific software for tax-ready records?

No. The IRS accepts any recordkeeping system, including spreadsheets and paper files, as long as records clearly show income, expenses, and supporting documents that substantiate your tax return.

How often should I reconcile my accounts to stay tax-ready?

Reconcile every bank and credit card account monthly. Completing reconciliations before making adjusting entries prevents timing errors and reduces the risk of rework during tax preparation.

What supporting documents do I need to keep?

Keep receipts, invoices, canceled checks, and bank statements organized by category. Each document should show the amount, date, vendor, and business purpose of the transaction.

Is tax-ready bookkeeping only necessary at tax time?

No. Tax-ready bookkeeping is a year-round practice. The IRS can review returns for up to three years after filing, so records must remain organized and accessible at all times, not just during tax season.